Tinubu’s $11.4 billion World Bank loans near Buhari’s eight-year total

President Tinubu’s administration has secured $11.4 billion in World Bank loan approvals in three years, nearing the $14.59 billio

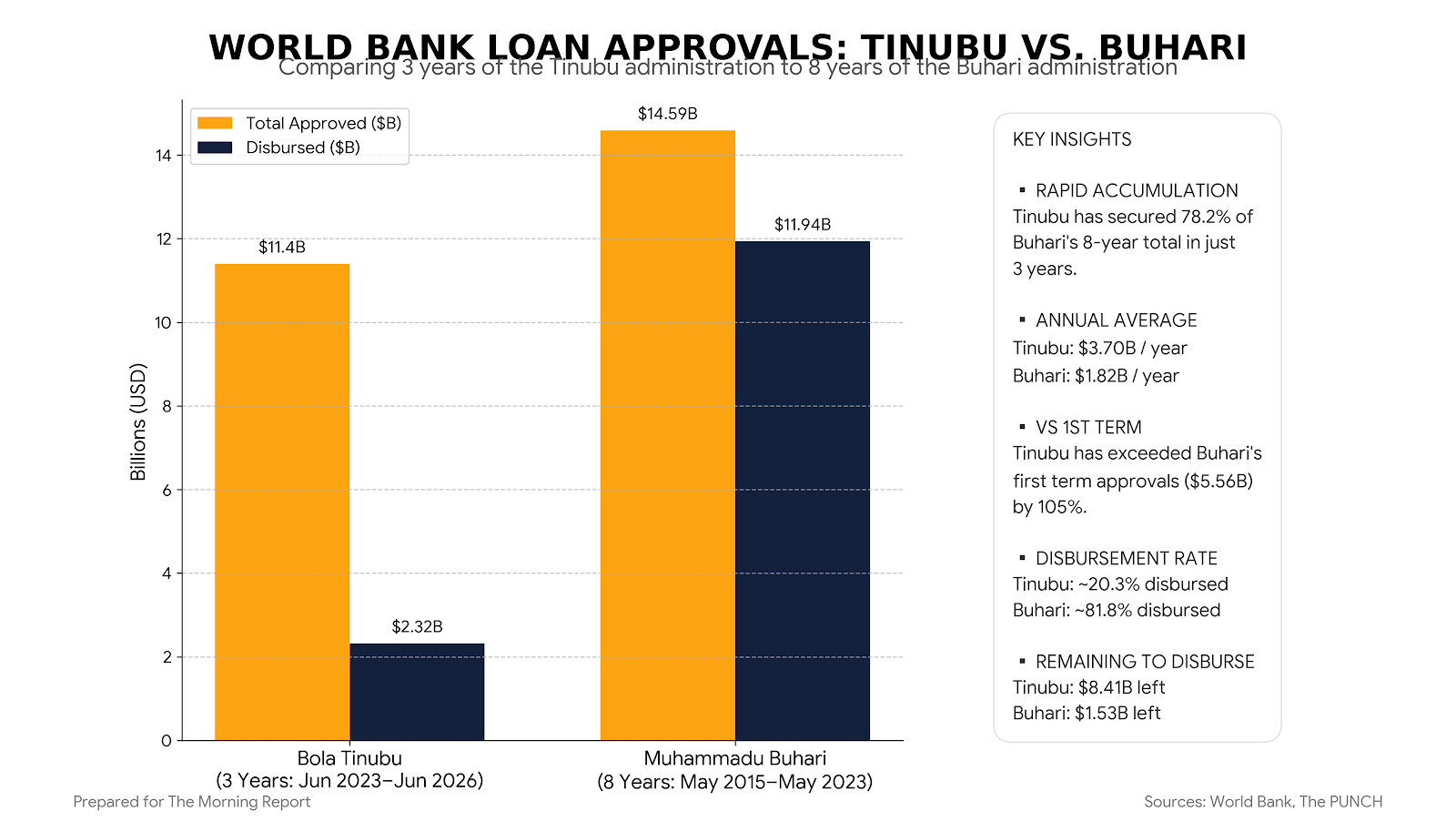

President Bola Tinubu’s administration has secured $11.4 billion in World Bank loan approvals between June 2023 and June 2026. That figure is on track to exceed the $14.59 billion approved during former President Muhammadu Buhari’s eight years in office, according to an analysis of World Bank data.

The approvals already represent about 78 percent of Buhari’s total, although only $2.32 billion, or 20.3 percent, has been disbursed so far. By comparison, 81.8 percent of loans approved under Buhari have been released. This means the Tinubu administration is borrowing faster but disbursing more slowly.

The funding supports economic reforms, power, agriculture, healthcare, education, digital infrastructure and social protection. Major approvals include a $2.25 billion reform package in 2024 and a $1.25 billion investment and jobs programme approved in June 2026.

Economists remain divided over the borrowing. Some argue concessional loans can support long-term growth if properly utilised. Others warn that rising debt and slow project implementation could increase fiscal pressure and debt-servicing costs.

This mirrors the borrowing spree of the Buhari era, which saw Nigeria’s debt stock rise from ₦12.6 trillion in 2015 to ₦87.3 trillion by the end of his tenure in 2023. The mechanism was different then, but the result was the same: borrowing to fund recurrent expenditure rather than productive investment. The slow disbursement rate suggests that even when loans are approved, the government struggles to spend the money effectively.

For the Nigerian taxpayer, the loans represent a future burden. The more Nigeria borrows, the more it must repay. With debt servicing already consuming about 90 percent of government revenue, the new borrowing adds to an already unsustainable fiscal trajectory.

The winners: the Nigerian government, which has access to cheap financing. The losers: future generations of Nigerians, who will inherit the debt, and the Nigerian economy, which must service the loans without necessarily benefiting from productive investment.

Bottom Line: $11.4 billion in three years. $2.32 billion disbursed. Nigeria is borrowing faster than it can spend. That is not a fiscal strategy. That is a debt trap.