REV360 data engine rewrites corporate tax compliance rules

Nigeria’s new digital tax system uses real-time data matching to enforce compliance, ending the era of manual desk audits.

Nigeria’s corporate tax system is undergoing its most significant transformation in decades. The Nigeria Revenue Service (NRS) has shifted from manual audits to real-time compliance, forcing businesses to rethink how they prepare tax returns, reconcile records and manage financial reporting.

The transition is driven by the newly integrated REV360 data engine, which combines mandatory electronic invoicing, expanded third-party data integration and automated risk assessment. Companies can no longer treat Company Income Tax (CIT), Value Added Tax (VAT), payroll taxes and banking records as separate compliance exercises. Instead, every filing is increasingly expected to tell the same financial story.

“The days of the casual, manual desk audit are officially over,” said Olanrewaju Phillips, former chairman of the Tax Appeal Tribunal. “With the transition to the Nigeria Revenue Service and the deployment of REV360, tax administration has become algorithmic. The authority is no longer waiting to visit your office physically; its systems are running automated cross-match checks on taxpayer information in real time.”

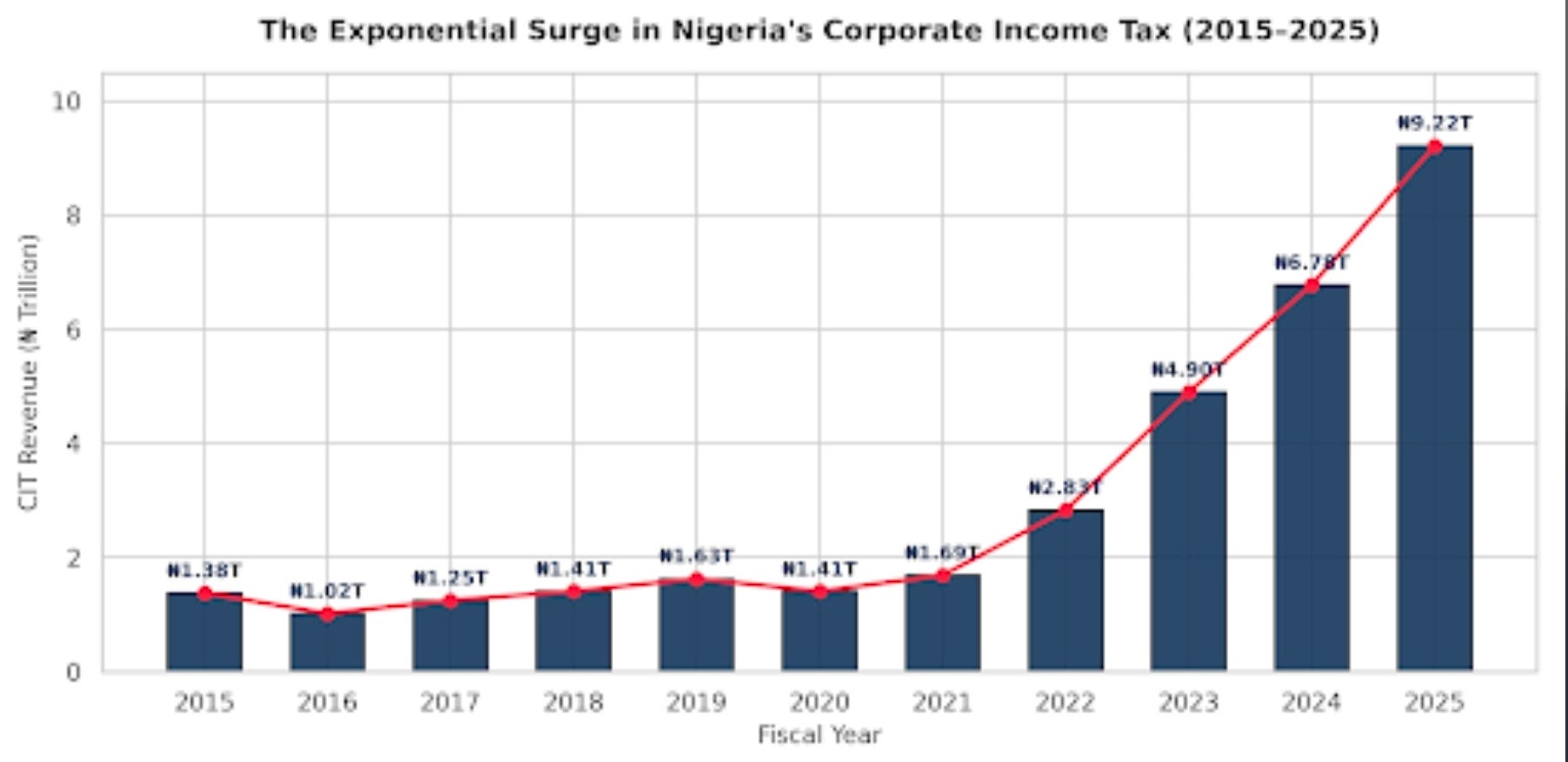

The development marks a broader shift in Nigeria’s revenue administration strategy, where compliance is increasingly driven by data analytics rather than traditional audit exercises. Tax experts say the approach is intended to improve voluntary compliance, reduce revenue leakages and expand the country’s relatively narrow tax base without necessarily introducing new taxes. The reforms come as the government pursues an ambitious target of increasing Nigeria’s tax-to-GDP ratio to 18 percent by 2027 from about 13.5 percent currently.

Taiwo Oyedele, chairman of the Presidential Committee on Fiscal Policy and Tax Reforms, recently disclosed that the number of individuals registered for tax purposes has expanded from about 10 million to more than 100 million, with thousands of informal businesses seeking registration daily as ongoing reforms encourage greater formalisation of the economy.

The changing architecture is also being reflected in revenue performance. Nigeria generated ₦2.42 trillion in value-added tax in the first quarter of 2026, representing a 17.06 percent increase from ₦2.07 trillion recorded in the corresponding period of 2025, underscoring stronger domestic economic activity and improving compliance.

For finance teams, the implications extend beyond filing deadlines. The NRS can now compare turnover declared in annual company income tax returns with monthly VAT submissions; identify inconsistencies between payroll expenses claimed for tax purposes and Pay-As-You-Earn (PAYE) remittances made to state tax authorities; and reconcile declared revenues with information obtained from third-party financial data sources. A mismatch that may previously have attracted little attention can now trigger automated compliance reviews, requests for clarification, delayed issuance of tax clearance certificates, or additional tax assessments where discrepancies remain unresolved.

“Before uploading any return, taxpayers should review their records using the same reconciliation logic the revenue authority’s systems employ,” Phillips said. “A detailed VAT-to-CIT reconciliation schedule explaining timing differences, exempt income, and legitimate accounting adjustments has become an essential compliance document rather than a best practice.”

The shift is occurring alongside the phased implementation of Nigeria’s Electronic Fiscal System (EFS), which has introduced mandatory electronic invoicing for large taxpayers with annual turnover of at least ₦5 billion, while medium-sized businesses will be required to comply mandatorily from 2026. Under the framework, business-to-business and business-to-government invoices require clearance by the NRS before they are issued to customers, with every qualifying invoice assigned a unique Invoice Reference Number.

A recent assessment by tax technology firm DigiTax noted that organisations operating across Nigeria, Kenya and Zambia must ensure their enterprise resource planning systems can automatically generate, validate, digitally sign and transmit invoices to tax authorities, warning that manual invoicing processes have become increasingly unsustainable under real-time compliance frameworks. The firm also advised businesses to validate supplier and customer tax identification numbers before invoice submission; establish procedures for handling rejected invoices promptly; and maintain structured electronic archives rather than relying solely on PDF copies, as tax authorities increasingly request machine-readable transaction data during compliance reviews.

This shift mirrors the 2010s banking sector reforms, when the Central Bank introduced electronic payment systems and real-time transaction monitoring. The mechanism then was different, but the result was the same: institutions that could not adapt were left behind.

The winners: businesses with robust accounting systems and stronger internal controls, which will face fewer compliance disruptions. The losers: businesses that continue to rely on fragmented records and manual reconciliation processes, which may find themselves increasingly exposed to automated audit triggers and enforcement actions.

Bottom Line: The tax man is no longer coming to your office. He is already in your systems. And he is watching.