Nigeria’s $2.7 billion food delivery boom struggles to turn a profit

Nigeria’s food delivery market is projected to reach $2.7 billion by 2034, yet profitability remains elusive as logistics costs crush margins and international players retreat.

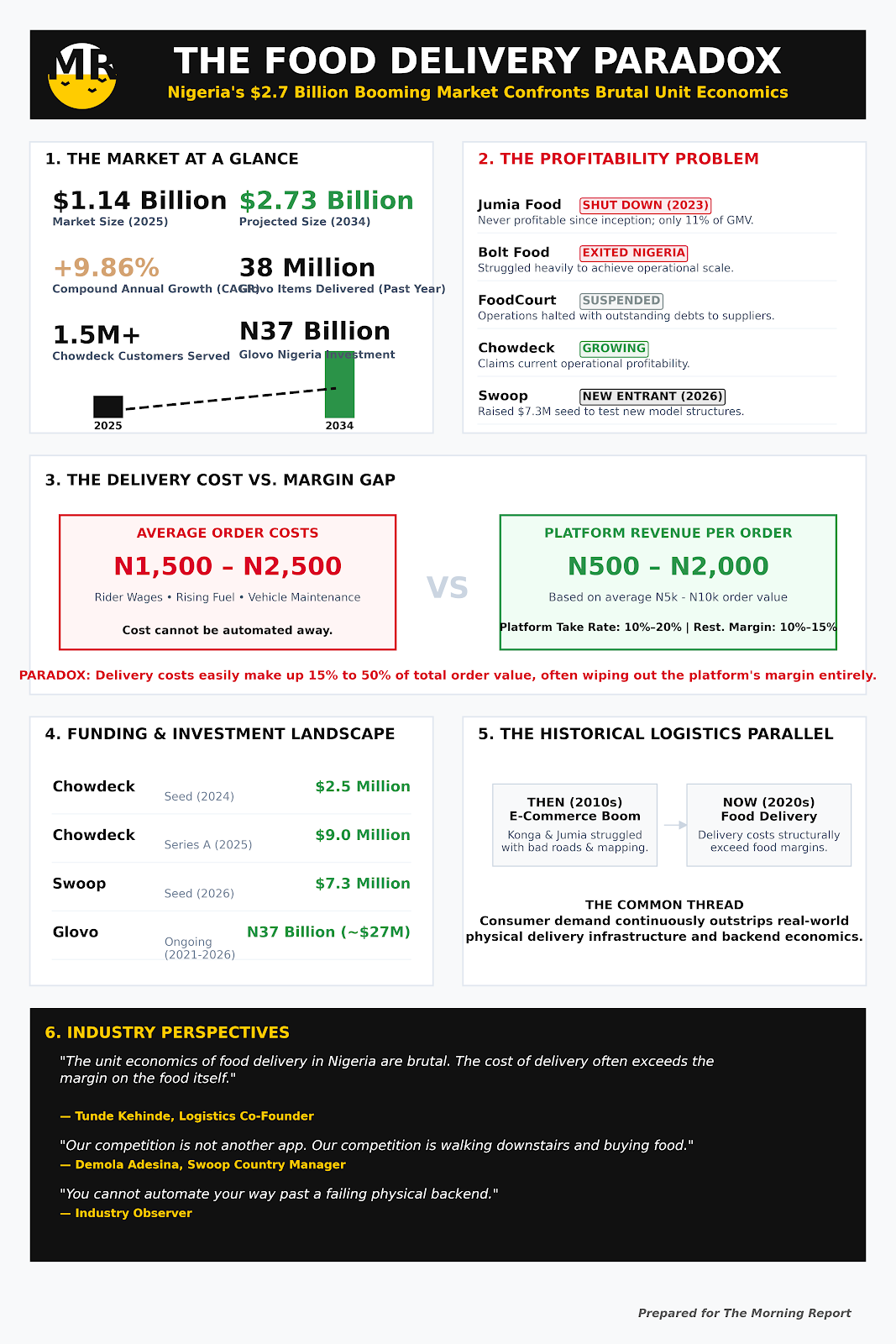

On paper, Nigeria’s online food delivery business should be one of Africa’s biggest technology success stories. The market reached $1.14 billion in 2025 and is projected to grow to $2.73 billion by 2034, expanding at a compound annual growth rate of 9.86 percent. Rapid urbanisation, rising smartphone penetration and a young population increasingly comfortable with online services continue to fuel expectations that ordering meals with a few taps on a smartphone will become an everyday habit. Food delivery, on the surface, seems like a business with almost limitless demand.

Yet beneath the impressive projections lies a very different reality. Over the past decade, Nigeria’s food delivery industry has produced as many business casualties as success stories. International brands with deep pockets have entered the market only to retreat. Local startups have struggled with rising operating costs, restructuring and unpaid obligations. Even companies reporting rapid growth continue to battle a question that has haunted the sector since its emergence: Can food delivery become consistently profitable in Nigeria?

The answer lies in a contradiction that defines the industry today. Demand is growing. Convenience is becoming part of urban culture. But making money remains remarkably difficult. Unlike software companies that can scale with relatively little additional cost, food delivery is a logistics business disguised as a technology company. Every order requires a rider, fuel, packaging, customer support, payment processing and real-time coordination. Each additional order generates additional costs, making profitability far more complicated than simply increasing the number of users.

That reality has humbled some of the industry’s biggest players. Nigeria’s modern food delivery business gathered momentum during the COVID-19 pandemic, when lockdowns accelerated demand for contactless shopping and home deliveries. International operators saw an opportunity. Jumia Food, originally launched as HelloFood around 2012, spent years building one of the country’s largest restaurant delivery networks. Bolt Food entered the market in 2021, hoping to leverage its ride-hailing ecosystem. Neither remained. By late 2023, Jumia shut down its food delivery operations across several African markets, including Nigeria. The food delivery business had not been profitable since inception and represented only 11 percent of Jumia’s gross merchandise value. Bolt Food also exited, choosing to refocus on its ride-hailing business after struggling to achieve the scale and profitability investors had hoped for.

More recently, FoodCourt, once celebrated for its cloud-kitchen model, entered a difficult period marked by operational disruptions, unpaid salaries and vendor complaints before announcing a restructuring programme. The Y Combinator-backed startup suspended operations after months of financial strain, with outstanding debts to suppliers and logistics partners becoming unsustainable. By April, its last remaining kitchen in Lagos had shut its doors entirely.

For those who have watched the industry’s casualties, the explanation is straightforward. Tunde Kehinde, co-founder of a logistics startup, described the fundamental problem in stark terms. “The unit economics of food delivery in Nigeria are brutal,” Kehinde said. “The cost of delivery often exceeds the margin on the food itself. You are essentially subsidising convenience.” His assessment is borne out by the numbers. The costs of fuel, maintenance, and riders' livelihoods cannot be automated away. As one industry observer put it, “You cannot automate your way past a failing physical backend”.

On the other hand, some analysts argue that the market is simply maturing. Wale Adeyemo, a partner at a Lagos-based venture capital firm, offered a more optimistic view. “Every new industry goes through a consolidation phase,” Adeyemo said. “The companies that survive will be the ones that crack the logistics puzzle.” He pointed to Chowdeck, which has emerged as a heavyweight in the space since its founding in 2021. The startup raised $2.5 million in seed funding in 2024 and followed with a $9 million Series A in August 2025. It now serves over 1.5 million customers across multiple cities in Nigeria and Ghana and claims profitability.

The optimists also point to Glovo, the global on-demand delivery platform that entered Nigeria in 2021. The company has invested over ₦37 billion ($27 million) in Nigeria and delivered 38 million items over the past year, nearly doubling the value generated for businesses on its platform. Nigeria emerged as Glovo’s fastest-growing market in 2025. Reni Onafeko, Glovo Nigeria’s general manager, described the company’s focus on empowering small and medium businesses with the tools and technology they need to compete in a rapidly evolving digital economy. Dima Rasnovsky, Regional General Manager at Glovo Africa, captured the bullish sentiment: “Nigeria has two things: population and momentum. It’s like a wave here, and it is great to be part of the journey”.

Yet even as some of the industry’s biggest names retreated, new investors are still betting that Nigeria’s food delivery market has room to grow. One of the newest entrants is Swoop, an Eswatini-born startup that launched operations in Lagos in 2026 after raising $7.3 million in seed funding. The company is taking a different approach from earlier entrants, focusing first on Lagos before expanding across Nigeria and eventually the continent. Demola Adesina, Swoop’s country manager, said Nigeria represents the company’s most strategic market because success here would provide the operational scale needed for continental expansion. “We are number one in Eswatini right now, and our goal is to be number one in Nigeria as well,” Adesina said. “If we hit that goal, it becomes easier to go across the continent”. The company charges what it describes as the lowest service fees in the industry and aims to ensure that food ordered through its platform costs nearly the same as buying directly from restaurants. “Our competition is not another app. Our competition is walking downstairs and buying food,” Adesina said.

Neutral observers offer a more measured assessment. Chidi Okonkwo, a tech analyst, noted that the industry is evolving rather than dying. “Food delivery is not dead in Nigeria. It is just taking a different shape,” Okonkwo said. “The winners will be those who focus on high-density urban areas and premium customers rather than trying to serve everyone at once.” Another analyst, Ngozi Eze, added: “The problem is not demand. The problem is the cost structure. Until someone figures out how to reduce delivery costs, profitability will remain elusive.”

This mirrors the 2010s e-commerce boom in Nigeria, when companies like Konga and Jumia attracted massive investment but struggled with the logistics of delivering physical goods across a country with poor roads and unreliable addresses. The mechanism was different then, but the result was the same: high demand, high costs, low profits.

The winners: consumers who enjoy the convenience of food delivery; riders who earn income from the platforms; and the few companies that manage to survive and scale, such as Chowdeck and Glovo, which are capturing market share while their competitors fall away. The losers: investors who have poured money into unprofitable ventures; employees of failed startups like FoodCourt; and the industry itself, which must prove it can be sustainable.

Bottom Line: A $2.7 billion market that cannot turn a profit is not a market. It is a subsidy. Someone is paying for the convenience. It is not the food delivery companies.