Government’s ₦34.5 trillion deficit pushes bond yields to 17.79%

The Federal Government’s record borrowing programme has pushed bond yields to 17.79%, as investors demand higher returns amid a surge in debt issuance.

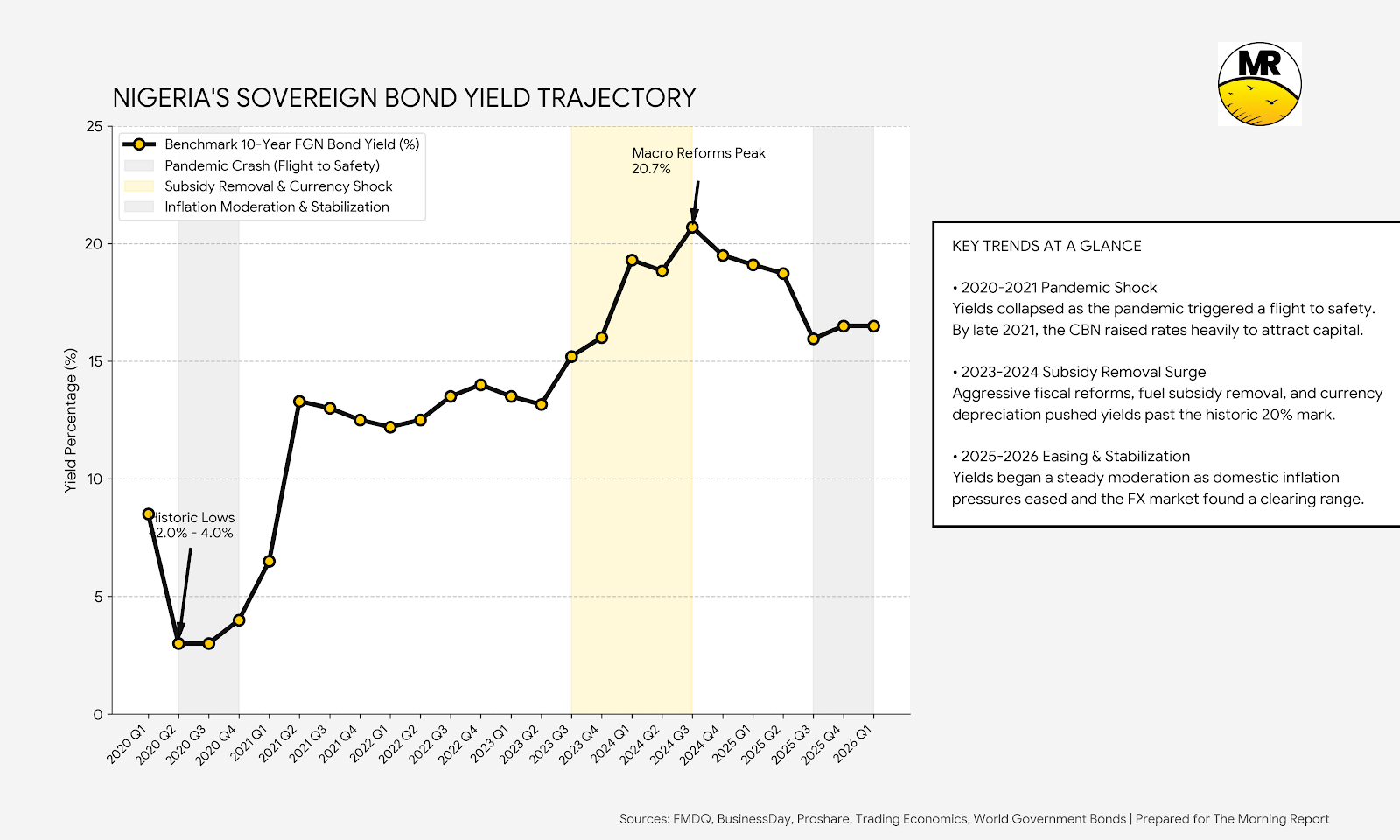

The Federal Government’s aggressive domestic borrowing programme has pushed up the cost of debt, as investors demand higher returns ahead of one of the largest sovereign debt issuances in Nigeria’s recent history. Average yields on Federal Government of Nigeria bonds rose by 148 basis points to 17.79 percent in June, driven by a sustained sell-off in the secondary market as investors priced in a significant increase in bond supply.

The pressure stems from the government’s ₦34.5 trillion fiscal deficit for 2026, with about ₦29.2 trillion expected to be financed through domestic borrowing. These expectations were reinforced after the Debt Management Office (DMO) issued ₦1.2 trillion in bonds at its June auction, the largest single auction on record. The DMO has since unveiled plans to raise between ₦3.8 trillion and ₦4.9 trillion in the third quarter, far higher than the approximately ₦2.5 trillion issued in the previous quarter.

The repricing has been felt across the yield curve. Medium-term bonds recorded the largest increase, with yields rising 158 basis points month-on-month, while short-term and long-term bonds rose 144 and 142 basis points, respectively. Marginal rates on the 2030 and 2032 maturities were also raised to 16.30 percent and 16.50 percent, up from 16.00 percent and 16.15 percent at the last auction.

The sell-off extended across the fixed-income market. Average yields on Nigerian Treasury Bills rose 103 basis points to 18.54 percent, while Eurobond yields rose 76 basis points to about 7.54 percent as global investors became more cautious amid renewed geopolitical tensions in the Middle East. Analysts said the sharp rise in domestic yields reflects investors pricing in the large volume of government paper expected to hit the market in the coming months.

Emmanuel Orji, a fixed-income trader, said the market is currently driven by two opposing forces: improvements in macroeconomic fundamentals and a sharp increase in government debt issuance. “Ironically, lower oil prices, while supportive of inflation, are also weakening government revenues,” Orji said. According to him, lower inflation and a relatively stable naira would ordinarily support lower bond yields, but the government’s expanded borrowing programme is likely to dominate market pricing in the near term. “When borrowing requirements become this large, investors regain pricing power,” he said. Orji expects bond yields to move towards, and potentially exceed, 19 percent during the third quarter as the market digests the increased issuance, before easing later in the year if inflation continues to moderate. He summed up the outlook by saying, “Supply pressure wins the auctions; fundamentals win the year.”

Not everyone believes the increase in government borrowing will immediately squeeze financing for the private sector. Titilayo Daramola, a fixed-income trader, said current yield levels are creating attractive opportunities for investors, while liquidity in the financial system remains strong enough to absorb the additional supply. “I believe it will create an attractive buying opportunity for investors and not crowd out the private sector just yet because there’s a lot of capital out there looking for where to be deployed,” Daramola said. According to her, robust subscription levels at recent government debt auctions indicate that investors still have ample liquidity to invest despite increased issuance. Daramola added that current yields remain below the highs seen earlier this year when Treasury bill discount rates traded above 20 percent, suggesting the market has previously absorbed even higher interest-rate environments.

Looking ahead, analysts expect supply pressures to remain elevated. In addition to the DMO’s planned bond issuance of up to ₦4.9 trillion in the third quarter, the Central Bank of Nigeria has scheduled ₦5.8 trillion in Treasury bill issuances for the period.

This mirrors the 2020 borrowing surge, when the government ramped up domestic borrowing to fund COVID-19 relief. The mechanism then was different, but the result was the same: higher yields, higher debt service costs, and a crowding out of private-sector investment.

The winners: investors who can now earn higher yields on government securities. The losers: the Federal Government, which will pay more to service its debt; the private sector, which faces higher borrowing costs; and Nigerian taxpayers, who ultimately bear the cost of the debt.

Bottom Line: The government is borrowing more, so investors are demanding higher returns. That is not a market failure. That is a market working exactly as it should. The question is whether the government can afford the bill.